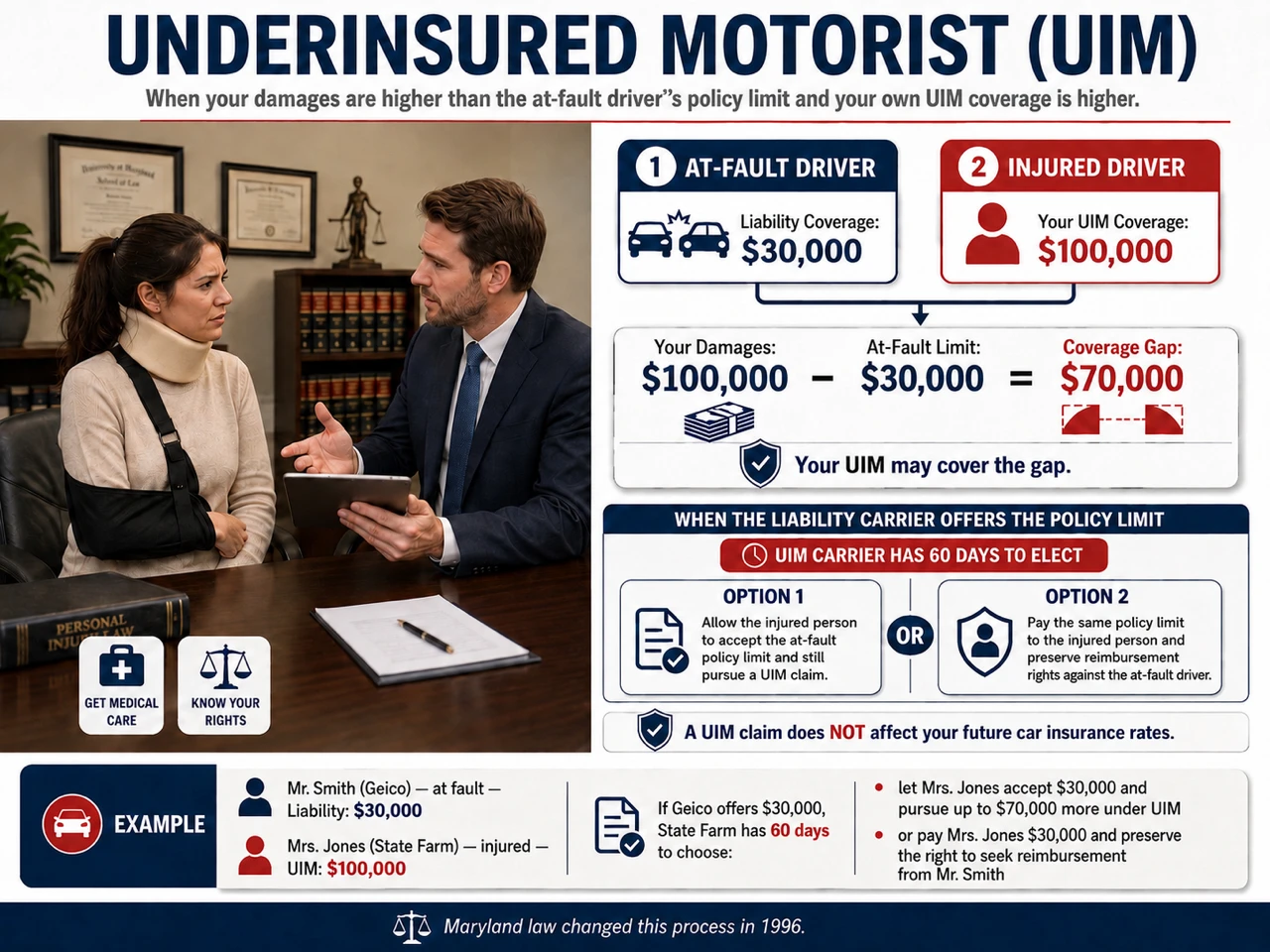

Underinsured Motorist

If the uninsured bodily injury coverage is greater than the at-fault driver's liability coverage.

Making such a claim will not affect your future car insurance rates. In those circumstances, the at-fault insurance carrier may offer their policy limit, but in return the injured party must sign a release which precludes anyone from further pursuing a claim against the at-fault driver. Historically, this meant that a claim could not be made against the injured person's uninsured carrier because the release precluded the carrier from seeking reimbursement from the at-fault driver. As a result, it was very difficult to resolve this type of claim. This was changed in Maryland by legislative enactment in 1996.

When the liability insurance company now offers the policy limit, the uninsured motorist company has 60 days after being placed on notice to make an election:

- The uninsured motorist carrier may either allow the injured party to settle for the policy amount while preserving the right of the injured party to make an uninsured claim

- The uninsured motorist carrier wishes to preserve their right for reimbursement against the at-fault driver, that carrier must pay to the injured party the policy limit offered by the at-fault driver's insurance company.

By way of example:

Mr. Smith has $30,000 of liability coverage through Geico and he is at fault in causing an accident. Mr. Jones sustains a serious injury from that accident and has $100,000 of uninsured motorist coverage with State Farm.

If Geico offers the $30,000 policy limit then:

- State Farm has 60 days to allow Mr. Jones to accept the $30,000 while reserving the right to pursue a claim of $70,000 against State Farm; or,

- State Farm can pay to Mr. Jones $30,000 and preserve their right to sue Mr. Smith for any verdict subsequently rendered above $30,000 up to $100,000.

Need our legal advice?

Call us for a free consultation

Slatkin & Lupo

Law Offices